China Outlook – Consumers key to breaking the deadlock

KEY POINTS

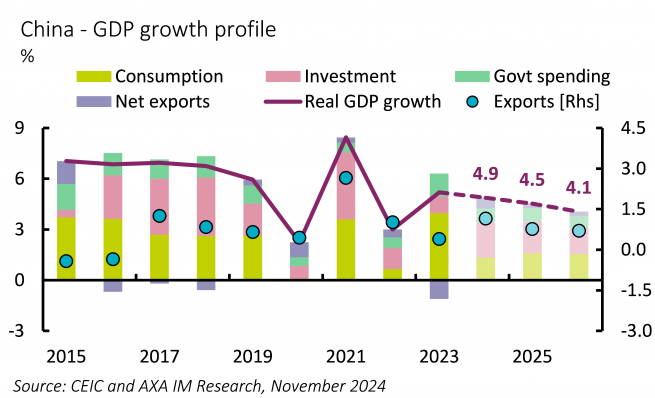

Another bumpy journey to target

For China, achieving its annual economic growth target remains the central performance measure for officials at all levels. The economy was well on track to meet 2024’s goal of “around 5%” by the end of the first half of 2024, largely due to robust momentum from state-led investment. However, this positive trajectory was disrupted as local governments, perhaps overconfident from initial progress, or constrained by mounting debt pressures, slowed investment at the start of the third quarter. This decision triggered a broad-based economic slowdown. In response, Beijing reiterated its commitment to the growth target, and the central bank implemented stronger-than-expected monetary easing measures in late September. As a result, the economy now seems poised to meet this year’s growth objective.

Looking back, 2024’s bumpy path evokes a sense of déjà vu. The post-pandemic reopening boost provided a strong start to growth in the first half of 2023. Yet, policy support fell short of sustaining that momentum as the reopening effect waned. To stabilise growth, Beijing was compelled to unleash additional stimulus in October, including a rare mid-year budget adjustment that benefitted infrastructure investment. Ultimately, the economy managed to achieve its target, expanding by 5.2%.

Many of the economic obstacles faced in 2024 carried over from 2023 and have since deepened further. To avoid a more material slowdown as domestic obstacles and external pressures look set to mount, China will remain heavily reliant on policy support. We foresee an ongoing need for additional fiscal stimulus and a shift in focus for its delivery – from production to consumer demand-centric. Assuming this, we predict a managed economic slowdown is ahead for China’s economy, forecasting growth of 4.5% in 2025 and 4.1% in 2026 (Exhibit 12). However, with Donald Trump’s return to the White House amplifying external risks and an already fragile domestic economy, a debt-deflation trap leading to a generational downturn could be perilously close if upcoming stimulus measures are delayed or misdirected.

Troubled consumers drag on the economy

Chinese consumers continued to struggle in 2024, as the triple impact of declining wealth, stagnating incomes and limited policy support underpinned entrenched pessimism.

Property prices continued their unprecedented adjustment, with average home values falling by 15% from their peak in the summer of 2021 – five percentage points (ppt) in 2024 – approximately a third of the total correction we estimated3. The shrinking value of property assets – where Chinese households have historically concentrated most of their wealth – has placed significant strains on domestic consumers. This compounded the fading post-pandemic reopening momentum in the labour market, further dampening consumer spending. Although headline unemployment figures indicated a mild improvement from 2023 levels, they provide limited insights into broader labour market dynamics. Wage growth throughout 2024 was particularly lacklustre. Following divergent trends in 2023, 2024 saw even lower-income earners face stalling wages. The pervasive slowdown in wage growth, combined with a pessimistic income outlook has led consumers to become increasingly cautious in their spending habits.

Moreover, Beijing’s policy focuses on largely overlooked household demand for much of the year. It was not until Q3 2024 that the government began to acknowledge subdued household spending and rising deflationary risks, though substantial quantitative measures were still lacking. As a result, a robust recovery in domestic demand is yet to emerge, as reflected in persistently low consumer confidence levels.

Stronger headwinds from abroad

By contrast, Chinese exports have maintained a good momentum, particularly since the second quarter of this year. This in part stemmed from front-loading demand, as foreign importers sought to avoid potential higher tariffs on Chinese goods as the US, the European Union, Canada and Indonesia all raised tariffs on Chinese goods in 2024. However, Trump’s return to the White House once again threatens a more hostile external environment for China.

We do not anticipate Trump’s proposed 60% blanket tariff on Chinese imports being fully implemented. During his 2016 campaign, despite his calls for a 45% tariff on Chinese goods, only 37% of the claim was ultimately enacted. The resulting decline in China’s exports to the US cut China's GDP growth by 0.6ppt, including the partial offset from currency devaluation – the Chinese yuan depreciated 5.2% against the US dollar. In Trump’s second term, we foresee a similar materialisation rate for the tariff policy relative to his campaign rhetoric. This would suggest a comparable tariff rise to that seen in the 2018-2020 period, with a similar impact on China's GDP, assuming similar currency adjustment behaviours.

- {https://www.axa-im.com/investment-institute/macroeconomics/macroeconomic-research/brick-brick-unravelling-chinas-property-puzzle;Wang, Y., “Brick by Brick: Unravelling China's property Puzzle”, AXA IM Research, May 2024}

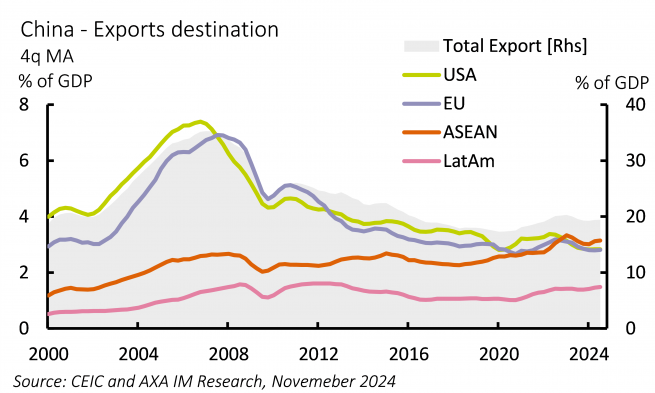

China has diverted its exports to other markets outside the US (Exhibit 13), and its integration into key global supply chains has deepened compared to 2018. These factors should offer some buffer against future potential US-China trade disruptions. It is worth noting the US’s broader trade policies with other countries could also have implications for China’s exports—harsher US trade stances globally may somewhat mitigate Chinese goods’ loss of competitiveness. Overall, we estimate that Trump’s anticipated trade policies will shave 0.3-0.5ppt off China’s GDP, although a large degree of uncertainty surrounds these projections.

Domestic spending may be the last resort

China’s investment-driven and export-supported growth model, which was instrumental in the nation’s remarkable growth over the past three decades, has long been a cornerstone of its economic policy. However, the conditions that once underpinned this success have shifted significantly. Although the recently announced RMB 10trn multi-year debt swap programme aims to alleviate mounting local government debt pressures4, returns on investment have diminished, constraining their ability to sustain expansion. Moreover, the golden era of infrastructure growth has slowed, reflecting the plateauing of urbanisation and a cooling housing market. While exports have transitioned to higher-value, technologically advanced goods, escalating trade tensions and shifting geopolitical dynamics present growing obstacles.

This places greater emphasis on China’s households, which hold substantial growth potential due to one of the world’s highest saving rates. With the right policies to revive the labour market and stabilise the property sector, a portion of these savings could be unlocked, albeit rebalancing the economy to a consumption-driven growth will take time. Beyond recent challenges, the elevated savings rate stems from an incomplete and limited social safety net, underscoring the critical need for structural reforms. Implementing such reforms could take decades, and it remains uncertain whether the government is willing to undertake such a transformative agenda.

We consider a revival of domestic demand through household-focused stimulus as the most viable path to achieving a managed slowdown and avoiding a pernicious economic downturn. The National People’s Congress meeting in March next year looks the most likely juncture for additional stimulus. In the interim, authorities may also encourage state-owned enterprises to support employment and promote better wage growth. It would not only help facilitate a gradual slowdown in China’s economic growth over the coming years but could also underpin a modest rebound in consumer prices. Alongside the support from a weaker yuan, we forecast inflation to rise from near deflation this year to 1.0% in 2025 and 1.6% in 2026.

- {https://www.axa-im.com/investment-institute/market-views/bonds-bridges-and-burdens-chinas-local-government-debt-focus;Wang, Y., “Bonds, Bridges, and Burdens: China’s Local Government Debt in Focus”, AXA IM Research, October 2024}

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.