How to generate performance in a credit portfolio

- 29 April 2025 (5 min read)

KEY POINTS

It has already been a tale of two cycles this year with the positive sentiment and stable growth experienced at the start of 2025 tumbling into inflationary and recessionary concerns. Trade tensions have been a dominant theme in recent weeks and are expected to persist in the coming months. In such an environment, looking for ways to create returns while mitigating risks are paramount for investors.

Fixed income is therefore a strong contender. Within this asset class, credit could be an attractive option as many companies have entered this unsteady period with strong balance sheets and sound fundamentals overall. Alongside this, absolute yields are still above levels seen for much of the past decade, maintaining some appeal. In Europe, credit should also benefit from falling rates, falling inflation and, albeit slow, growth. Overall, we think there are strong reasons to consider credit within a portfolio.

Generating performance from credit, particularly in challenging markets, isn’t always straightforward. Fortunately, there are many levers to pull especially if taking a flexible approach that aims to identify sources of value, take advantage of market anomalies, and adapt to market fluctuations.

We use a robust investment process to select issuers across sectors, regions and credit ratings. The process is important as issuer selection can improve or detract from the overall performance. Alongside return considerations, the allocation across these different factors helps provide diversification, mitigate credit risk and reflect best ideas within a portfolio.

Sector allocation

Different sectors will respond differently to market conditions. Typically, when economies are slowing or during times of stress, we expect defensive sectors (eg utilities and telecoms) to perform better than cyclical sectors (eg automotives and capital goods) as they are less likely to be impacted by an economic slowdown. For example, the market’s response to the US tariffs was one of heightened risk aversion. In this environment, defensive sectors were more resilient, showing smaller moves compared to the greater volatility seen in cyclical sectors.

Credit allocation

Credit ratings indicate the likelihood of an issuer defaulting on its payments. If a bond is investment grade, it will have a high credit quality rating because it is considered less likely to default on its payments and, therefore, seen as less risky. High yield bonds, on the other hand, have a lower credit rating but tend to offer higher income in return.

Creating the right balance between investment grade for credit risk mitigation and high yield for enhanced income returns can be a strong performance driver. Our total return strategy, for example, maintains flexibility across credit market, with a historical average allocation to high yield of around 30% since inception1 , while preserving an overall investment grade credit profile.

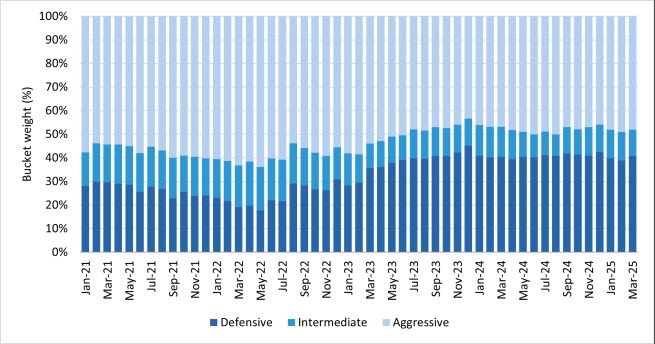

In order get the most from our asset allocation, we divide the investment universe into three risk categories defined according to the fundamentals and characteristics of the markets in which we invest.

- Defensive: This includes cash equivalent and very high-quality corporate bonds from core European countries such as France and Germany. This risk bucket is generally quite defensive and offers low volatility and high liquidity characteristics

- Intermediate: Corporate bonds that are still highly rated but in European countries considered periphery such as Italy and Spain. This bucket should provide more yield opportunities and a little more volatility

- Aggressive: High yield and subordinated bonds across the different geographic regions which should provide high levels of yield but also increase the amount of volatility

By investing flexibly and dynamically in these three pockets of risk depending on the market environment, we aim to generate solid risk-adjusted returns.

- U291cmNlOiBBWEEgSU0gYXMgb2YgMjV0aCBBcHJpbCAyMDI1LiBJbmNlcHRpb24gb2YgQVhBIElNIEV1cm8gQ3JlZGl0IFRvdGFsIFJldHVybiBzdHJhdGVneTogMjZ0aCBGZWJydWFyeSAyMDE1

Duration

Interest rate risk is an important consideration in bond portfolios. Short duration bonds – typically bonds with one-to-three years maturity – are less sensitive to interest rate changes than bonds with longer maturities. This is because long duration bonds which often have maturities of 10 years or more, are more vulnerable to interest rate changes due to the uncertainty of future economic conditions and interest rate environments.

The ability to manage duration allows us to adjust the portfolio’s interest rate sensitivity, aligning it with both current market conditions and longer-term trends. For instance, in a declining rate environment, we can aim to capitalise on price appreciation by increasing exposure to long-duration bonds. Conversely, in a rising rate environment, we should be able to mitigate potential losses by favouring short-duration bonds. This strategic flexibility gives us the opportunities to optimise portfolio performance while seeking to provide valuable downside protection in periods of interest rate volatility.

Volatility has the final word

The word volatility can bring dread to an investor’s heart as it suggests slumps in returns. However, what is often overlooked is that volatility can also offer opportunities. We welcome volatility, as it allows us to implement our views much more dynamically than in a sluggish market. A flexible management approach should enable us to capitalise on market overreaction, buying when others may be selling in panic. In this way, we see volatility not as a risk, but as an opportunity to enhance returns.

Disclaimer

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, AXA IM HK, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2025 AXA Investment Managers. All rights reserved.