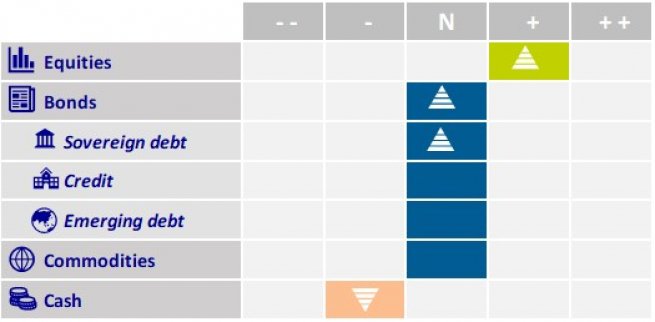

Multi-Asset Investments Views: Cut Me Deep

KEY POINTS

Federal Reserve (Fed) Chair Jerome Powell was very clear in describing the central bank’s shift of focus, from inflation to employment, and from balanced to downside risks when he spoke at the Fed’s annual seminar in Jackson Hole, Wyoming in August. He said: “It seems unlikely that the labor market will be a source of elevated inflationary pressures anytime soon. We do not seek or welcome further cooling in labor market conditions.”

He continued: “The upside risks to inflation have diminished. And the downside risks to employment have increased.”

Still, the Fed managed to surprise on the dovish side less than a month later on 18 September by cutting interest rates by 50 basis points (bp), instead of the 25 expected. With US GDP growth around 3% annualised for the third quarter of 2024 (according to the Atlanta Fed’s Nowcasting model) and job creations still in positive territory, some analysts view this double-cut decision as precipitated and even as a policy mistake. As investors, we do not need to judge the merits and flaws of this decision, and merely take stock of its implications: the so-called Fed put is back. In plain English, this expresses the market confidence that US monetary policy will ease, not just when faced with a major systemic shock but also in a pre-emptive fashion to cushion any concerns of an economic slowdown.

Top-down macroeconomic indicators are rather reassuring and bottom-up corporate earnings have encouraging perspectives with upside revisions in the US, especially compared to somewhat softer expectations. More importantly in our view, the signs of market complacency we flagged entering the summer are now gone. First, the soft landing narrative (in which the US economy only goes through a mild slowdown and avoids a recession despite the tremendous tightening in monetary policy) is no longer as consensual.

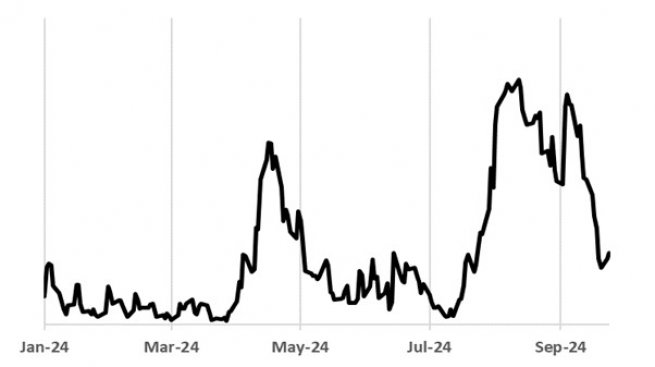

Second, the implied volatility for the options market – i.e. the expected movement in option prices - rose sharply in August and has only partly reversed since then, illustrating that investors remain mindful of risks. For example, the VIX – also known as the fear index - which corresponds to the implied volatility on the US stock market, remains above 15, while it was below 13 in May and June.

We favour our proprietary composite indicator of systemic stress (CISS), a broader, cross-asset volatility measure inspired by the European Central Bank’s (ECB) own CISS.

Lastly, many investors reduced their asset allocations significantly in August and early September. Positive momentum is building up again and we are monitoring the risk of valuations increasing as investors return to the market but we find that we are not quite there yet.

August and September saw what we believe to be the start of the broadening of the global stock market rally. With interest rates moving sharply lower, we see potential opportunities in rate-sensitive equities in the US and Europe, from US small caps to European real estate (REITs). Elsewhere however, we are concerned Japanese equities could suffer from the yen appreciation with the Bank of Japan taking a diverging hiking path and carry trades still at risk of further unwinding.

Lacklustre momentum in the Eurozone economy presents challenges for large-cap stocks there - in particular, the luxury goods and autos sectors face significant headwinds, including China’s structural slowdown. While China announced a massive monetary stimulus package to support its own equity market and address some of the negative impacts of its real estate crisis on the economy, the measures announced might still fall short of restoring an entrenched consumer confidence. Contrary to the US where we see some overreaction to the ‘growth scare’, we find no such comfort for the Eurozone where recessionary risks are still credible.

On the fixed income side, the market quickly moved to price in the inflation normalisation and then moved further to account for the risk of a significant economic slowdown. The US 10-year interest rate has fallen rapidly from 4.7% in late April, to almost 3.6% in September.

Most of that adjustment reflects an extreme repricing of the Fed’s willingness to cut interest rates. The short end of the US yield curve is now consistent with almost 200bp of cuts over the next 12 months. We believe any positive news on the macroeconomic front, for example an upside surprise on US non-farm payrolls, would spark some upside consolidation for yields.

The uncertain outcome of the looming US presidential election can also influence investors’ expectations for the long end of the curve. We therefore believe patience on duration exposure is warranted, with potentially better entry points later this year. If anything, we favour sovereign bonds in Europe (Germany, Spain, UK) rather than the US or Japan.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.