US reaction: FOMC still sees three cuts as inflation outlook not really changed

- 21 March 2024 (3 min read)

KEY POINTS

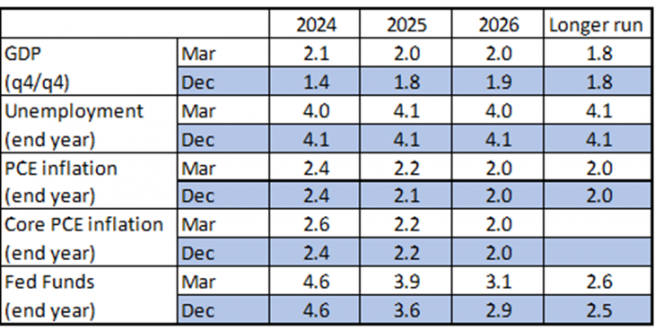

The Federal Reserve left policy rates unchanged at its March meeting, the Fed Funds target range at 5.25-5.50% and interest on reserve balances at 5.40%. The Fed continued with its current pace of QT. These decisions were by unanimous decision, as broadly expected. The Fed’s short-term outlook as described by its accompanying statement was barely changed. The statement removed the description that jobs growth had “moderated since early last year”, simply stating that “gains have remained strong”. There was more adjustment to the Summary Economic Projections (SEP) (see Exhibit 1 below). Growth expectations were raised for this year (end-year forecast raised to 2.1% from 1.4% in December), in part reflecting an expectation of ongoing momentum from the fast close to last year and stronger labour supply. However, future years growth was also edged higher to stay at 2.0% in subsequent years – ahead of the Fed’s assessment of trend growth. However, the Fed’s unemployment forecast was barely adjusted, bouncing around the Fed’s view of the long run rate. Core PCE inflation forecasts were also raised for this year to 2.6% from 2.4% in December, but forecasts continued to show headline (and core) inflation returning to the 2.0% target in 2026, with headline inflation edging higher to 2.2% (from 2.1%) next year.

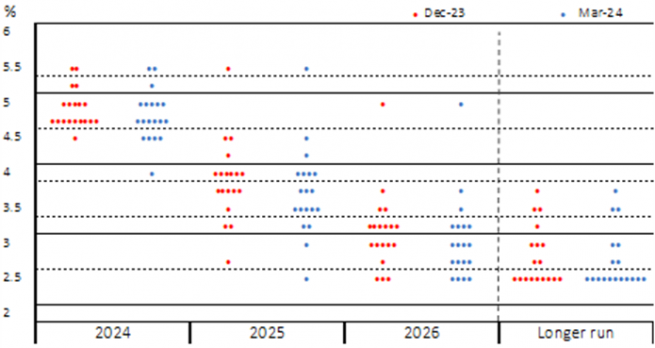

Most importantly, the median rate outlook of the Committee continued to see three rate cuts for 2024. Exhibit 2 illustrates that in turn the median stability disguised a modest adjustment in the distribution of the Committee’s views: more participants considered policy with fewer than three cuts this year and fewer saw more, but the majority of the Committee continued to expect three or more cuts over the year. However, expectations for cuts in 2025 were reduced to 75bps (from 100bps) and 2026 still saw 75bps, but now to 3.25-3.00% from 3.00-2.75% in December. The median rate outlook for the long-term rate also increased to 2.6% from 2.5%, with the central tendency widening to 2.5-3.1% (from 2.5-3.0%). All suggests that the Fed’s confidence in the longer-term easing it will need to deliver has reduced, even if its short-term outlook has been less effected.

Fed Chair Powell’s press conference broadly addressed the current market zeitgeist: that higher inflation at the start of the year would derail the Fed’s expectations of rate cuts for this year. Powell was measured and consistent saying that the Fed needed more data to have sufficient confidence to ease policy. He said that January and February’s data had not added to that confidence, but nor did he think it had changed the picture. He repeated that the Fed would “approach the question carefully”. The Fed Chair reiterated that inflation had made “substantial progress”, but more was needed. He concluded that the ‘dots’ showed that most members expected to have sufficient confidence to “begin to dial back the level of restrictiveness .. at some point this year”. Separately, the Fed Chair went someway to explaining the change to the Fed’s SEP outlook of firmer growth but no meaningful change to unemployment by highlighting stronger labour supply.

Our own view is for now unchanged. We continue to expect to see some moderation in services inflation over the coming months to provide sufficient confidence for the Fed to begin cutting in June, but acknowledge that that case has yet to be made by the data. We continue to forecast four cuts for this year – rather more than the Fed and markets now consider. This view sees the Fed quickening the pace of cuts by year-end. Our own view is that the economy is likely to be a little softer than the Fed’s current outlook and we think the Fed will accelerate cuts as softness becomes apparent. However, we acknowledge that this cut is in the balance and a firmer growth outlook could see us shift this view. We still expect the Fed Funds Rate to close 2025 at 3.75-3.50%, now below the FOMC’s projections. We also do not think that the timing of Fed cuts will be impacted by this year’s Presidential election, with no evidence that it has been impacted by elections over the past four decades.

The Fed Chair also revealed that the Fed had started to discuss tapering the pace of QT at this meeting. He explained that the Fed believes that by reducing the balance sheet more slowly it will allow a more even distribution of reserves between banks and could avoid liquidity issues, in turn potentially allowing the Fed to ultimately reduce reserves further. This is the argument Dallas Fed President Logan advanced at the start of the year. Powell said that the Fed would make a decision on the slower pace “fairly soon”. Since Logan’s comments at the start of the year we have expected the Fed to announce a slowing of the pace (broadly to halve the pace) in June, effective in July. We maintain this view, but acknowledge the risks of an announcement at the next meeting.

Market reaction was mixed. Short-end rates pared back fears that short-term inflation prints had derailed Fed rate cut expectations. The probability of a June cut rose to 84% from 68bp before the release and December’s pricing gained 9bps, to see the probability shift from three cuts by year-end not being fully priced to now seeing a chance of more than 25% of four cuts. 2-year UST yields dropped 7bps to 4.61% and the dollar fell by 0.5% against a basket of currencies. Stocks also received the news well, particularly the outlook for stronger growth, but still an easing in short-term policy and the S&P 500 equity index gained 0.9% on the release setting a new record high in excess of 5200. However, 10-year UST yields were more concerned about fewer rate cuts further out and the prospect of the Fed mulling a higher LR FFR. 10-year yields initially fell to 4.23% from 4.28%, but then revered to rise to 4.32% before settling at 4.27% at the time of writing, just 1bp lower.

Disclaimer

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, AXA IM HK, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2025 AXA Investment Managers. All rights reserved.