How a short-term view may improve long term prospects

KEY POINTS

Short duration bonds can often have a role to play in an investor’s portfolio regardless of the market cycle. However, with the current macro backdrop, we think there are now even more reasons why investors may wish to consider short duration strategies.

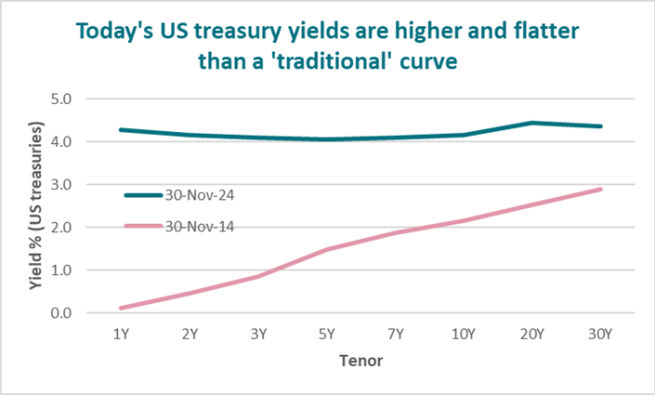

Today, US yield curves are higher and flatter than historical levels. For investors, as the chart shows, the current level of yield and flatness of the curve helps make fixed income an attractive asset class. This is especially true for short duration where investors can find similar yield levels to longer duration but with potentially less interest rate risk.

With opportunities across fixed income, particularly credit, short duration potentially presents a route that may provide attractive total returns while mitigating interest rate risk. Of course, short duration is not one homogenous asset class and, as such, offers a range of outcomes for a different investor needs.

We have split these main investor outcomes into five categories, however in practice the outcomes are not mutually exclusive and many of the investment offerings can offer two or more of these outcomes.

Step out of cash

For investors looking to enhance cash returns, taking an intermediate step into riskier assets via the short duration part of the curve could be an option. As rates fall and cash is no longer king, short duration strategies, with their typical maturities of up to three or five years, should offer a suitable bridge between cash holdings and longer-term fixed income investments. This is because they allow for harnessing income, while mitigating the impact from rates or spread volatility.

In order to achieve this step, one option could be to consider regional strategies such as US, Euro and Sterling short duration credit. This is because these asset classes have large investable universes that should appeal to investors moving out of cash due to their high liquidity and diversification characteristics.

However, for those who do not want to make regional allocation decisions, a global approach may be more appropriate. This approach allows investors to find broad exposure across region and sector allocations and so presents the potential of further opportunities but is also a potentially lower risk strategy due to its global and diversified nature.

Go For Growth

Short duration strategies could act as a tool to generate positive total returns in an uncertain environment given the natural income generating component of these bonds combined with expected bond price increases as rates come down. Short duration bonds within asset classes such as high yield or emerging markets may therefore be an option to help investors access higher income and growth while still mitigating against interest rate risk.

This is particularly the case for US high yield short duration strategies which should benefit as the high positive carry of the asset class helps to offset any drawdowns , while benefitting from the ongoing resilience of the US economy keeping a lid on credit spreads. As the most liquid part of the US high yield market, this strategy may also offer investors higher liquidity as well as being a complement to other asset classes. The chart below shows the total returns of the short-dated US High yield market over the last 10 years compared to the short dated US investment grade and US cash returns.

The short duration Euro high yield market could also offer an attractive proposition, with the higher all-in hedged yield levels offsetting the weaker economic environment in the Eurozone versus the US.

Diversifier

While the benefits of core short duration strategies such as investment grade credit and high yield bonds are clear, there remains an often-overlooked group of strategies for investors seeking upside in returns, but with a reduced correlation to traditional fixed income assets, thereby enhancing risk-adjusted returns.

Inflation-linked bonds (ILBs) are an example of a type of bond that tends have a lower correlation to other fixed income asset classes or stocks. This is because the coupons and principle payments of an ILB tends to increase with inflation, contrasting to other asset classes where the value decreases when inflation rises. The table below demonstrates this with 1-5 Year Global Inflation-linked Bonds having a relatively low correlation to other fixed income strategies, particularly corporate bonds.

Correlation across fixed income asset classes

Indices: ICE BofA 1-5 year global inflation-linked government index, ICE BofA Global Government Index, ICE BofA US Corporate index, ICE BofA Euro Corporate index, ICE BofA US High Yield Index, ICE BofA Euro High Yield Index

At the moment, while it is unclear how many of the policies Trump will implement in full, we expect to see some tariff increases, restricted migrant flows and moves towards a fiscal easing package during 2025. This could result in both supply shocks and a demand boost, both of which would be inflationary. Short duration inflation-linked bonds could provide an effective hedge against inflation, low exposure to interest rate volatility, and a low correlation to other fixed income assets.

Another way to consider diversification is through broadening regional exposure. For example, shorter-term Asian USD bonds currently offer relatively higher spreads than similar-maturity US peers and a broader country risk diversification. The diversity of Asian businesses and economies should give investors exposure to credits that are less prone to US trade policies. Economies such as India are also much more domestically orientated sheltering the issuers from geopolitical volatility.

Dynamic allocation

In periods of uncertainty and greater volatility, moving dynamically across regions, sectors and asset classes may help provide investors with opportunities. For 2025, with Trump’s presidency expected create potential headwinds beyond the US, the continuing geopolitical challenges across the Middle East and Ukraine, and expected divergence in central bank’s monetary policies, many investors may look to a flexible approach as it provides the potential to exploit opportunities available in the global short-dated fixed income universe via active asset class and sector allocation as well as active management of duration across currencies.

Short duration offers portfolio managers a cheap and easy way to refresh portfolio holdings through the natural liquidity pipeline from bonds maturing. This ability should therefore help them take advantage of different market environments. It could be particularly relevant when there are dislocations between government and investment grade or high yield and emerging markets, as well as when there are opportunities to move across the short end of the curve.

For those investors seeking the flexibility to adapt to changing market conditions throughout the cycle, a global approach to short duration may be one option as it offers access to the broad short-dated universe in order to exploit opportunities.

Responsible Focus

Investors targeting net zero objectives can also do this through short duration strategies without compromising on returns. When reflecting responsible investing in a portfolio, there are two main approaches to consider:

- Carbon transition strategies. These strategies focus on seeking opportunities associated with the transition to a low-carbon economy and gradually reducing exposure to carbon emissions. For investors, it offers a means to reflect concrete action within an investment portfolio that supports the transition to a lower carbon economy.

- Green bonds. Green bonds finance projects that are focused on a positive environmental impact and that ultimately contribute to the transition to a low carbon economy. These projects can be quite broad but the majority sit within one or more of these environmental themes: green buildings, sustainable ecosystems, low carbon transport and smart energy solutions.

The growth of the green bond universe means that it has moved from being considered a niche investment to a part of a global aggregate portfolio. This increased diversity means investors have different routes to access this asset class including through short duration bonds.

Both of these approaches can be accessed through short duration strategies.

Many short duration outcomes

While riskier than cash, the potentially higher returns on offer, limited drawdowns and natural liquidity of short-dated bonds, we believe, make them an attractive consideration for an investor’s portfolio.

At AXA IM, we have managed short duration strategies for 25 years and have a wide range of short duration strategies. We believe we are, therefore, well placed to discuss how short duration can offer investors different outcomes depending on what they are looking for.

So, whether the outcome is diversification, responsible investing, growth or being able to take a flexible approach, short duration may offer a path to that outcome.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, AXA IM HK, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2025 AXA Investment Managers. All rights reserved.